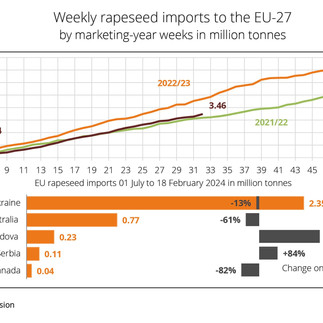

BLE has confirmed what was felt by all market traders that not only Biofuels usage has reached a plateau as feedstock choices have increased GHG of Biofuels efficiency dramatically causing Germany to continue to become a major biodiesel exporter (2.7 Mil MT in 2023 up from 2.34 Mil MT in 2022) despite increased mandate to 8%. We also note that RME gross margins continue to narrow ($210/mt) as we experience a rebound in vegoil prices. Although, this writer believes this rebound, particularly for RSO will be temporary until new crop as imports of Rapeseed are 13% lower than last year with Australian origin being the most significant change (only 768kt this year Vs last year 2.0 Mil Mt).

Comments